Investing in Trust: Enduring Growth of the Global Cybersecurity Market

Examining the Drivers Behind Two Decades of Resiliency (2004-2024)

Executive Summary

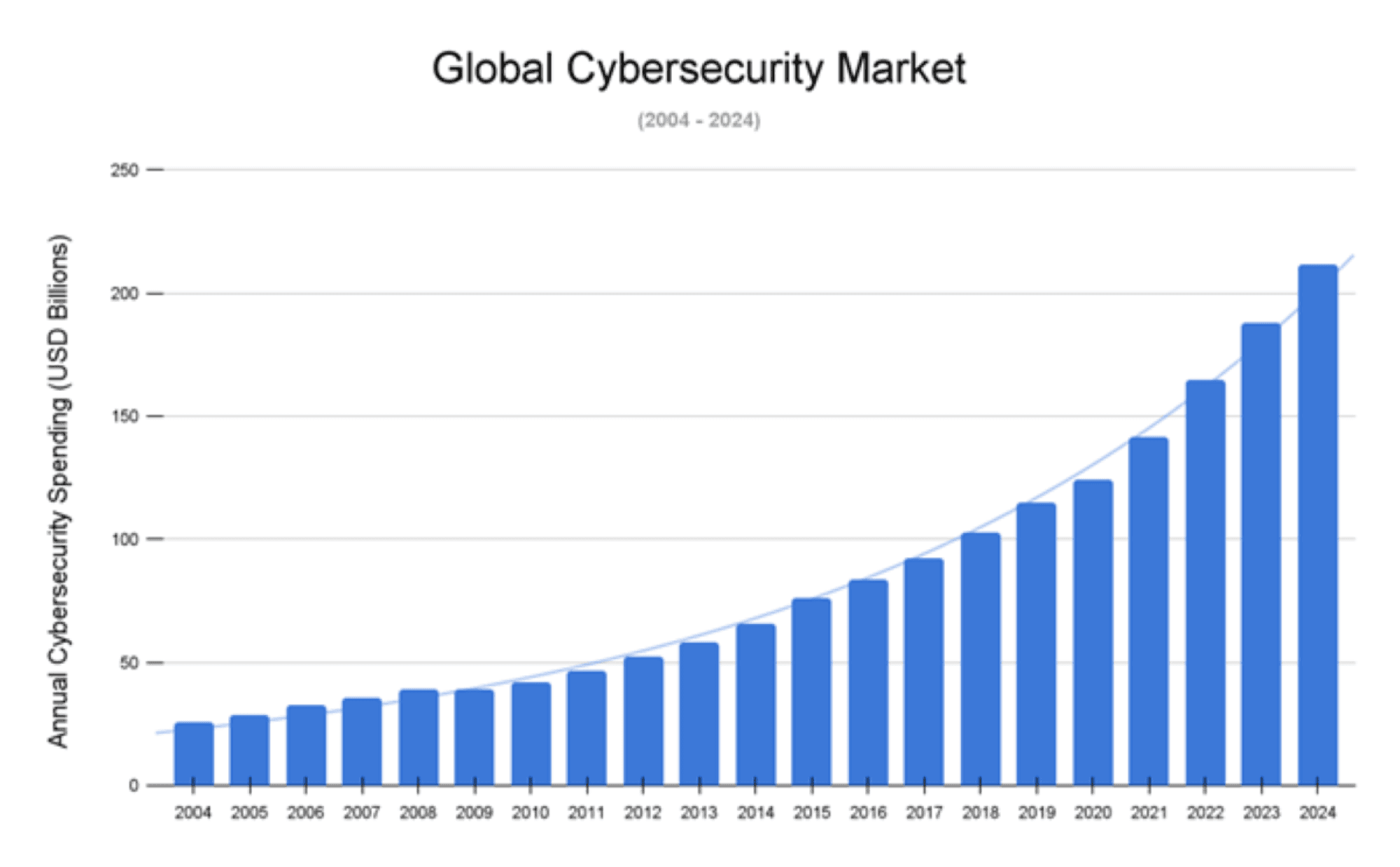

This report examines historical global cybersecurity market spending on products and services from 2004 through 2024 with a specific focus on how spending has fared during periods of economic recession. Drawing upon data and forecasts from leading market research firms including Gartner, IDC, and Forrester, the analysis reveals a dramatic growth trajectory over the two decades. The market has evolved from a nascent sub-segment of information technology (IT) in the late 1990s, estimated at just a few billion dollars, into a major global industry exceeding $200 billion in annual spending in 2024.

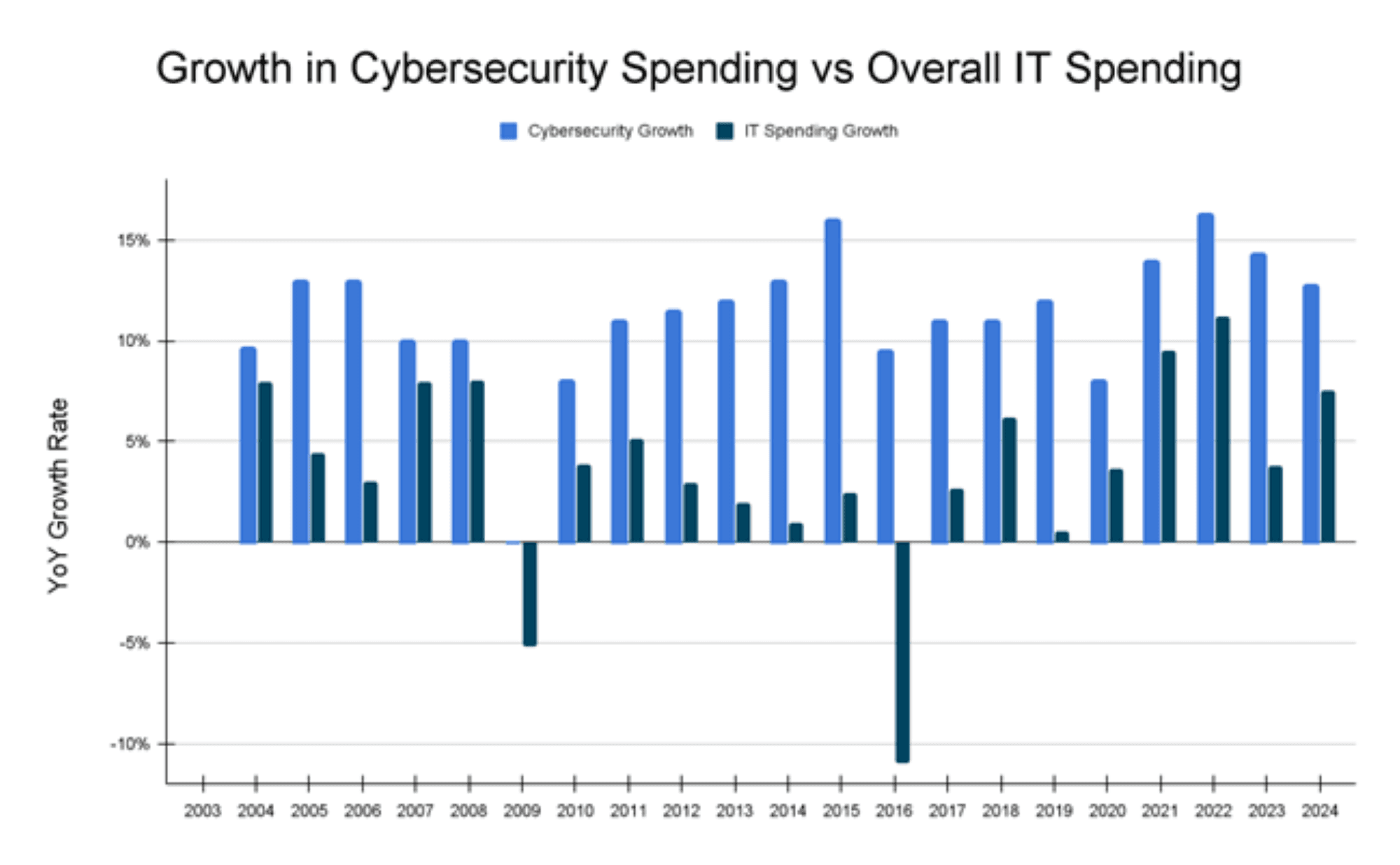

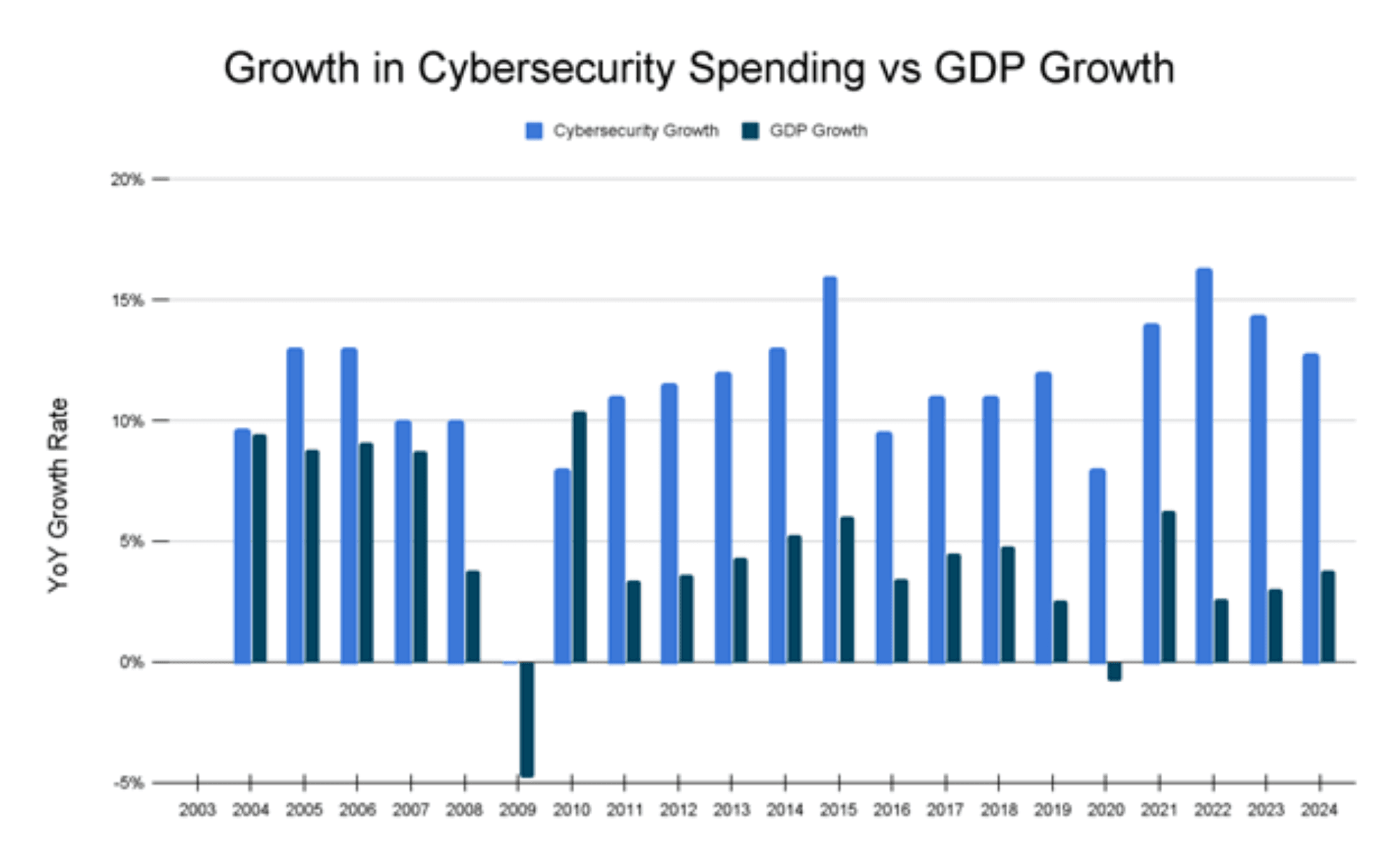

A key finding of this analysis is the market's consistent expansion, which has frequently outpaced the growth of overall IT spending. Most notably, the cybersecurity sector has demonstrated remarkable resilience during significant global economic downturns. Analysis of spending patterns during the Great Recession (2008-2009) and the COVID-19 Recession (2020-2021) indicates that cybersecurity spending continued to grow, or experienced only minor deceleration, even as broader economic activity and general IT budgets faced contraction. This cycle-independent strength points towards a fundamental shift in how organizations perceive cybersecurity – moving beyond a discretionary IT cost towards an essential component of business risk management and operational continuity.

Looking ahead, forecasts for the next decade indicate continued robust, double-digit growth for the global cybersecurity market. This sustained momentum is fueled by a confluence of powerful drivers. These include the relentlessly escalating sophistication and frequency of cyber threats, particularly ransomware and supply chain attacks; the ongoing digital transformation initiatives across industries, heavily reliant on cloud computing and increasingly incorporating Artificial Intelligence (AI); mounting regulatory pressures mandating stricter data protection and security postures; and the growing C-suite recognition that robust cybersecurity is not merely a defensive measure but a critical enabler of trust and business innovation in the digital age.

Introduction

In an era defined by pervasive digitalization, cybersecurity has transcended its origins as a technical niche to become a required cornerstone of the global economy. The operational reliance on interconnected systems, the exponential growth of data, and the migration to cloud computing have created unprecedented opportunities but also exposed organizations to a dynamic and increasingly hostile threat landscape. The financial and reputational consequences of cyber incidents are escalating dramatically, with global cybercrime costs projected to amount to trillions of dollars in 2025 (according to Forrester research), dwarfing the economic impact of natural disasters and rivaling the GDP of major nations. This stark reality serves as a primary catalyst for the consistent growth in global cybersecurity spending observed over the past two decades.

Given this backdrop, this report illuminates how investments in cybersecurity are influenced by broader economic cycles, with a particular emphasis on the resilience and vulnerability of this spending during recessionary periods.

The Evolving Landscape of Global Cybersecurity Spending (2004-2024)

The journey of global cybersecurity spending over the past two decades reflects the broader digital transformation of society and the economy. From a relatively small, technically focused niche, it has grown into a strategic imperative for organizations worldwide. This evolution can be understood by examining distinct periods characterized by different growth drivers, market maturity levels, and responses to global economic conditions.

Foundational Years (mid ‘90s - 2007): Early Market Formation

Driven by the first wave of internet commercialization, this period marked the formative years of the cybersecurity market as a distinct entity. While the need for IT security (a market subsequently renamed “cybersecurity”) existed, spending was often reactive and fragmented, primarily focused on point solutions like anti-virus software, firewalls, and intrusion detection systems to address nascent internet threats. Obtaining consistent, specific global spending figures for cybersecurity during this period is challenging, as market tracking often aggregates security within broader IT or ICT (Information and Communications Technology) categories. However, a crucial benchmark for this early era comes from the leading market intelligence firm IDC. In their December 2005 Report “Worldwide IT Security Software, Hardware, and Services 2005-2009 Forecast: The Big Picture”, estimated the global cybersecurity market size at $23 billion in 2003.

Resilience Through the Great Recession (2008-2009): Cycle-Independent Strength

The global financial crisis of 2008 and the subsequent Great Recession exerted significant pressure on corporate and government budgets worldwide. Overall IT spending faced headwinds; Gartner, for instance, projected substantial declines for 2009, initially forecasting a 3.8% drop, later revising it to a 6% decline from 2008 levels. This contrasted sharply with the strong 8% growth seen in 2008.

Amidst this widespread budget trimming, the cybersecurity sector exhibited remarkable resilience. A pivotal data point published in June 2009 by Gartner indicated that global spending on security software (a subset of the cybersecurity market), grew by an impressive 18.6% in 2008. Gartner noted,

“In 2008, the security market did not show any noticeable impact from the economic downturn. A double-digit growth in a challenging economic climate shows that security remains a key priority for CIOs and IT security leaders.”

Investment banking firm Cowan & Company stated in their January 9, 2009 research note,

“Overall the [IT security] sector continues to sound relatively resilient with resellers, distributors and others close to companies indicating that security remains relatively sheltered from budget cut-backs.”

Even in the depth of the recession, IDC anticipated a flat year for IT security in 2009 after 12% growth in security spend in 2008, to be followed by a resumption of growth in 2010.

Several factors likely contributed to this cycle-independent behavior. Economic downturns historically correlate with an increase in certain types of crime, including fraud and cybercrime, as financial pressures mount. Indeed, the FBI reported a 22.3% increase in online crime complaints in 2009 compared to 2008. This heightened threat environment likely compelled organizations to maintain or increase security investments to protect critical assets. Furthermore, new regulations introduced during this period and a growing understanding of the potentially crippling costs associated with breaches shifted security spending from a discretionary category towards a mandatory operational necessity.

Decade of Expansion (2010-2019): Mainstream Growth

The period from 2010 to 2019 witnessed the transformation of cybersecurity from a specialized concern into a mainstream business priority. This substantial market expansion was fueled by accelerating digitalization across all sectors of the global economy, the proliferation of mobile devices, the nascent and then rapidly expanding adoption of cloud computing, and a steady stream of high-profile data breaches that dramatically increased awareness of cyber risks at the board level.

While overall IT growth was often in the low-to-mid single digits (and sometimes negative in USD terms due to currency shifts [2016]), cybersecurity spending consistently outpaced this, driven by its increasing strategic importance. On average, spending grew 12% annually during this period.

Beyond technological shifts like cloud and mobile, the evolving regulatory landscape played a significant role in driving security spending. From 2004, when the Sarbanes-Oxley Act made cybersecurity a board-level mandate, new regulations related to data privacy and breach notification in various jurisdictions and vertical industries required enhanced security measures, fueling further investment.

The threat landscape also grew more complex, moving beyond simple malware to more sophisticated targeted attacks and the rise of organized cybercrime syndicates.

Navigating the COVID-19 Pandemic (2020-2022): Digital Acceleration, Heightened Risk

The onset of the COVID-19 pandemic in 2020 triggered unprecedented global disruption, including significant economic uncertainty and a dramatic, almost overnight shift to remote work for a vast portion of the global workforce. This created a complex environment for IT spending. Initial forecasts projected sharp declines; Gartner, for example, initially predicted an 8% drop in overall global IT spending for 2020, later revising this to a decline of 5.4% to 7.3%. However, the pandemic also acted as a massive catalyst for digital transformation, accelerating cloud adoption and reliance on digital services. This led to a strong rebound in overall IT spending in 2021 and 2022, with growth rates reported between 8.4% and 9.5%.

Within this volatile context, cybersecurity spending demonstrated continued strength, driven by factors directly exacerbated by the pandemic. The rapid shift to remote work vastly expanded the corporate attack surface, dissolving traditional network perimeters and increasing reliance on potentially insecure home networks and personal devices. Simultaneously, cybercriminals exploited the heightened anxiety and disruption caused by the pandemic, launching waves of phishing scams, ransomware attacks, and campaigns targeting critical infrastructure such as healthcare. The FBI's Internet Crime Complaint Center (IC3) recorded a 69% jump in cybercrime complaints from 2019 to 2020, rising to over 791,000 reports. It is widely acknowledged that these figures likely represent only a fraction of the true volume of attacks, as many incidents go unreported.

Evidence suggests that despite potential budget pressures elsewhere, organizations recognized the increased cyber risk and prioritized security investments. Several surveys indicated most organizations planned to increase cybersecurity spending in response to the pandemic. Spending growth estimates for cybersecurity during this period generally remained positive, with figures suggesting around 7% growth in 2020 and accelerating to approximately 14% in 2021. Technologies enabling secure remote access (like VPNs) and providing visibility into distributed environments and cloud platforms saw particularly strong demand.

The pandemic experience expanded cybersecurity's role beyond just threat defense and compliance. It became evident that robust security was a prerequisite for enabling the accelerated digital transformation forced by the crisis – supporting remote workforces, securing cloud migrations, and ensuring business continuity. This wasn't merely a temporary reaction to a crisis; it represented a fundamental shift, cementing cybersecurity as an indispensable component of modern, resilient business operations. This further reinforced its strategic importance and provided strong justification for sustained investment, even amidst economic uncertainty.

Current Market Dynamics and Future Outlook (2023-2030)

The world has moved beyond the pandemic and the cybersecurity market continues its strong growth trajectory, driven by persistent threats, business imperatives, ongoing digital initiatives, and new technological paradigms like Generative AI (GenAI).

Recent Market Size (2023-2024): Establishing the Current Baseline

In a series of reports in 2023, IDC forecast that worldwide security investments (hardware, software, services) would reach $187.5 billion in 2023 and $211.4 billion in 2024 marking a 12.1% annual growth rate. This growth was notably projected to outperform overall IT spending growth for the same years. Supporting this picture of increased investment, a Moody's survey highlighted that organizational spending on cybersecurity surged between 2019 and 2023, with cybersecurity's share of the total IT budget rising from 5% to 8%.

Spending Forecast (2025 and beyond): Continued Double-Digit Growth

Given its crucial role in ensuring business continuity and mitigating increasingly sophisticated cyber risks, cybersecurity investments are now considered essential. Furthermore, regulatory pressures and the need to maintain customer trust further solidify the resilience of cybersecurity budgets. From surveys of IT leaders, cybersecurity consistently emerges as a top priority for organizations, with many planning to increase their spending in this domain. Surveys also indicate that within the overall IT budget, cybersecurity projects would be the least likely to be cut.

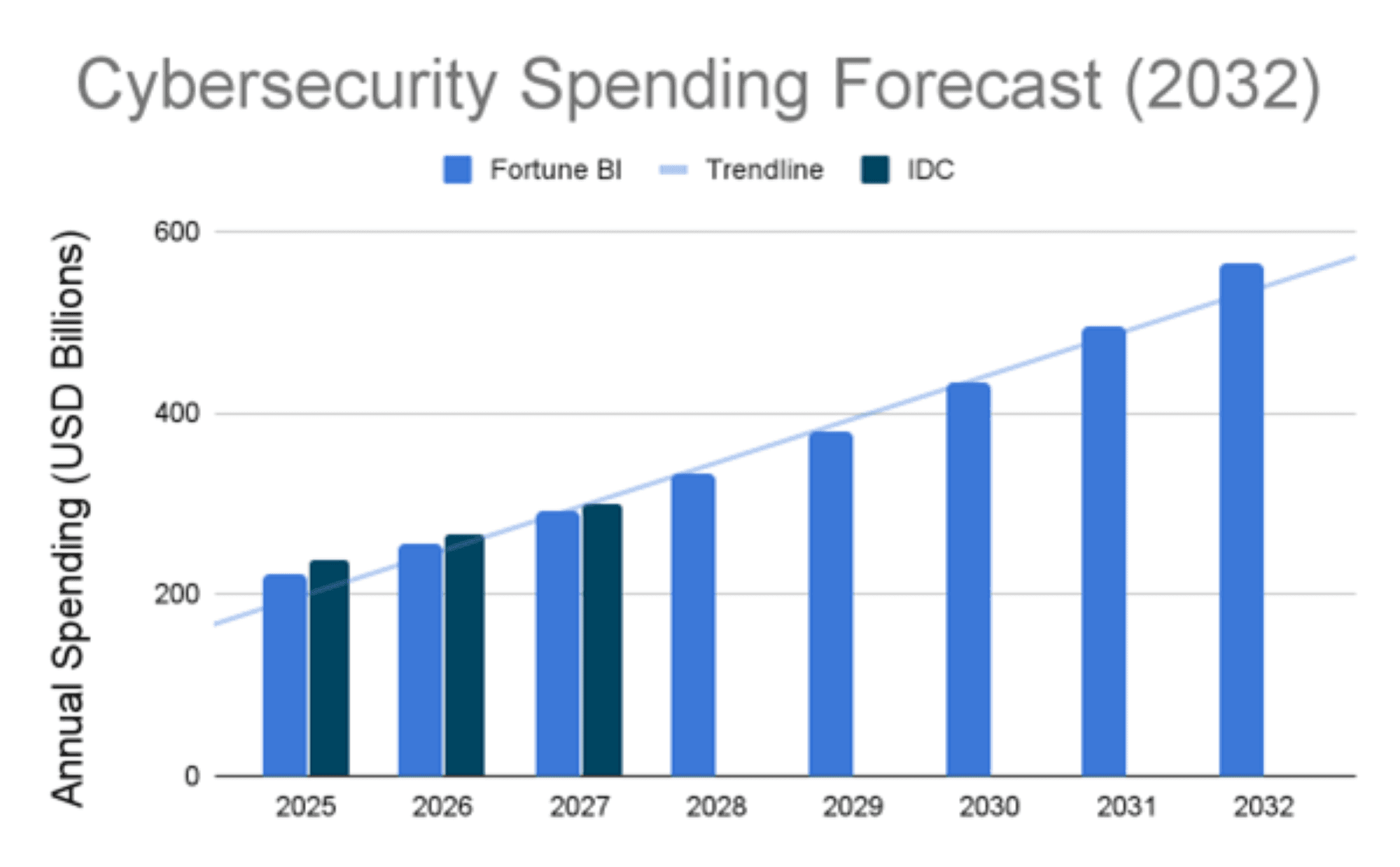

For 2025, cybersecurity remains a critical area of increasing investment. Forrester predicts continued growth in spending on cybersecurity solutions. Gartner also underscores the high priority of cybersecurity, forecasting a 15% rise in global spending for 2025. IDC anticipates an 11.8% growth in European security spending and a 12.2% increase worldwide.

Beyond 2025, most forecasts for global cybersecurity spending consistently project robust double-digit growth. Notably,

IDC forecasts global cybersecurity spending to grow at 12.8% CAGR to reach $300 billion for the year 2027. IDC Security Spending Guide, July 2023

The global cybersecurity market size was valued at USD 172.24 billion in 2023 and is projected to grow from USD 193.73 billion in 2024 to USD 562.72 billion by 2032, exhibiting a CAGR of 14.3% during the forecast period. Fortune Business Insights, Cybersecurity Market Analysis - 2032

Key Growth Drivers: Threats, Technology, Regulation, and Labor Scarcity

The sustained high growth and resiliency in cybersecurity spending will continue to be propelled by a confluence of factors:

Persistent and Evolving Threats: The threat landscape remains highly active and is constantly evolving. Ransomware continues to be a major concern, with attacks growing in sophistication and financial impact. The advent of accessible Generative AI (GenAI) introduces new threat possibilities, such as more convincing phishing attacks or AI-powered malware, necessitating new defensive strategies.

Technology Adoption & Transformation: The ongoing migration to cloud environments necessitates significant investment in cloud-native security tools and expertise. The integration of AI across business functions requires securing AI models and data, while also leveraging AI and automation within security operations for threat detection, response, and efficiency gains. Cybersecurity is increasingly viewed as a critical enabler for broader digital transformation initiatives, ensuring the security and resilience of new digital services and customer experiences.

Regulatory and Compliance Mandates: Expanding data privacy regulations (like GDPR, CCPA, and others globally) and industry-specific compliance requirements impose stringent security obligations on organizations, driving investments in data security, privacy solutions, and governance frameworks.

Cybersecurity Skills Shortage: The persistent global shortage of skilled cybersecurity professionals forces organizations to invest more heavily in security services (e.g., consulting, managed services) and automation technologies to augment their internal capabilities and bridge talent gaps.

The emergence of AI presents a particularly complex dynamic. While it clearly drives new security spending needs – both to defend against AI-powered attacks and to secure organizational AI deployments – it also promises significant productivity gains through automation within security operations.

Conclusion and Insights from TechOperators

For the last quarter century, a defining characteristic of the cybersecurity market has been its consistent growth and, crucially, its resilience in the face of economic volatility in major downturns. Unlike many other areas of IT spending that experienced sharp contractions during the 2008-2009 Great Recession and the initial shock of the 2020 COVID-19 pandemic, cybersecurity spending continued its upward trajectory.

This cycle-independent behavior stems from a confluence of factors. The threat landscape consistently intensifies. Furthermore, the relentless pace of digital transformation has made secure operations a non-negotiable prerequisite for business continuity and competitiveness.

Increasingly stringent regulatory mandates related to data privacy and security also compel ongoing investment, regardless of the economic climate. This market resilience underscores a fundamental shift:

Cybersecurity is no longer viewed merely as an IT tool but as an essential component of enterprise risk management and a critical enabler of digital business strategy.

Looking ahead, the factors driving cybersecurity spending are set to intensify. The proliferation of AI technologies presents a double-edged sword: creating new attack vectors and methods for adversaries while simultaneously offering powerful new tools for defense and automation. Securing AI systems themselves, along with the vast datasets they consume, will become a major focus. The continued migration to multi-cloud and hybrid environments necessitates sophisticated cloud security solutions. The persistent global cybersecurity skills gap will continue to fuel demand for managed security services, consulting, and automation technologies that can augment overburdened internal teams. Market consolidation is also likely to continue as larger platform vendors acquire specialized capabilities and customers seek to reduce vendor complexity.

The cybersecurity market has undergone a profound transformation over the past two decades. Here at TechOperators Venture Capital, our careers span this market. Having been founders and executives of some of the industry’s leading companies our team manages our investments in the next generation of market leaders. This is our wheelhouse and we're excited to invest in the innovations powering the enduring growth and resilience of the cybersecurity market.

Related

Insights

More Operator Insights.